Despite its best intentions, Bitcoin and other cryptocurrencies are no longer the discrete and anonymous digital assets they used to be. Paying your crypto tax, while complicated, is a necessary process that protects you from difficult situations with regulators like the IRS down the line.

It’s no secret that virtual currencies like Bitcoin and Ethereum are witnessing exponential adoption worldwide. The number of crypto holders continues to grow yearly, increasing by 39% in 2022 alone.

Sponsored

Unfortunately, cryptocurrency tax reporting is still a labyrinthine mystery for taxpayers. Are all profits made from crypto trading counted as capital gains or ordinary income? Do all my cryptocurrency transactions count as taxable events?

This crypto tax guide will answer all your basic questions and hopefully prepare you for the next tax year.

Why is Cryptocurrency Tax So Complex?

If most of your crypto activity happens on Binance or Coinbase, you shouldn’t have too much trouble. These large crypto exchanges provide plenty of comprehensive tax forms, documents and tools that simplify your tax preparation.

However, the world of blockchain and crypto assets is a deep and dark rabbit hole. The deeper you go, the more complicated your tax return becomes. If you’re actively involved in DeFi, you’re probably earning extra taxable income through staking or airdrops. Some traders also have multiple wallets.

What’s more, not every trade is as simple as swapping fiat currency for crypto. If you’re flipping NFTs or trading crypto-to-crypto, you must always keep records of your purchase prices. Calculating your holding period is also crucial because that can influence whether your profits will be considered short-term or long-term capital gains.

Finally, every country is different. There is no global crypto tax software or income tax rates. What is true for the IRS in the United States is very different from what you can expect in Dubai or Singapore.

What Does the IRS Say – Capital Gains Tax or Income Tax?

Given that the United States has some of the highest adoption rates of cryptocurrency in the world, the rulings of the IRS are often followed by local taxation entities in other countries. According to the IRS, cryptocurrency is considered a capital asset, like property.

What this means is that any crypto gains or losses need to be treated as a taxable event. In crypto trading, this is deemed a capital loss or a capital gain, based on whether or not you profited from the event. On the other hand, any cryptocurrency earned from staking, mining, or airdrops is treated as income and is subject to income tax. This includes any crypto acquired from network hard forks, as we saw during the Ethereum Merge.

Not All Cryptocurrency Transactions Are Taxable

If you’re looking at your wallet history and starting to panic, don’t worry! Some crypto transactions don’t need to be registered on your tax filing. These common activities are not treated as taxable events by the IRS:

- Purchasing virtual currency like Bitcoin or ETH using fiat currency.

- Moving crypto between your own wallets.

- Donating cryptocurrency for charitable reasons.

- Offering crypto to others as a gift.

Any crypto gifting under the value of $15,000 typically has no tax implications for the gifter. However if the receiver chooses to sell the gift, that will be considered a taxable event. It’s essential to keep records of the asset’s fair market value and the gifter’s purchase price. This is also called a cost basis.

Donating crypto to a charity is a great way to spread goodwill and makes the donor eligible for a tax deduction. This deduction is typically equal to the fair market value of the capital asset at the time of the donation.

Crypto Tax Brackets

Apart from the few exceptions listed above, most transactions, whether on a cryptocurrency exchange or in DeFi and NFTs, are taxable events. These include, but are not limited to :

- Selling crypto for fiat currency or trading one virtual currency for another.

- Paying for goods and services using cryptocurrency.

- Earning crypto through mining, staking or airdrops.

- Getting your income paid for in cryptocurrency.

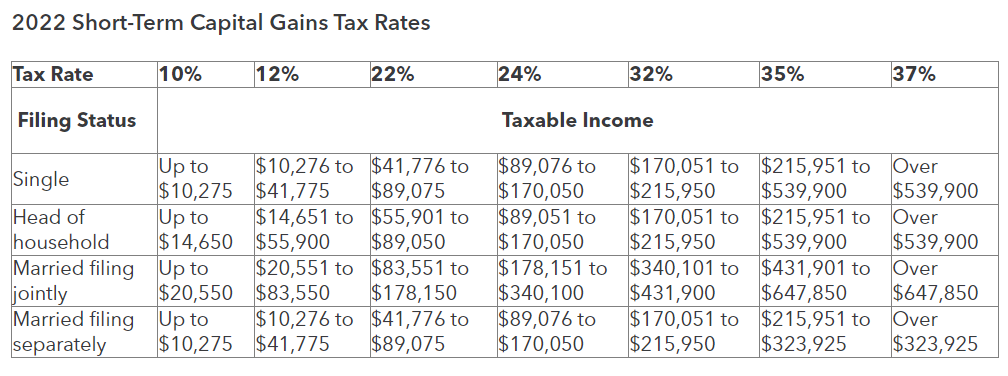

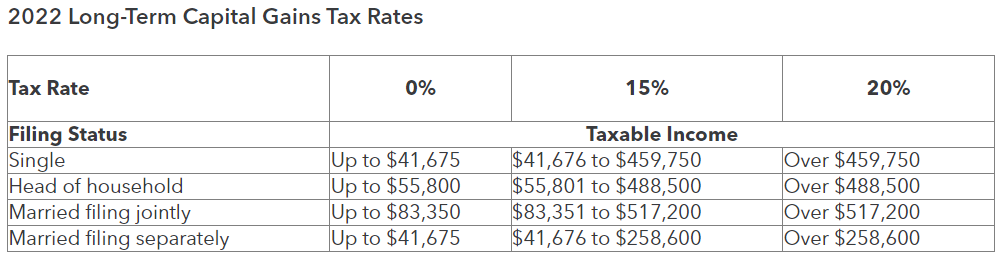

Like in traditional taxation and finance, the amount of crypto tax you’re required to pay depends on how much you’ve gained through income or capital gains. For assets that you’ve held for less than one year, short term capital gains or losses will apply. If you’ve HODLed for over one year, your assets will be treated as long-term capital gains.

Your tax bracket is determined by your overall income, with different rates applied depending on whether each taxable event is considered a long-term or short-term holding period. To give you an idea of what you can expect, TurboTax provides a helpful chart outlining the different brackets.

TurboTax also offers a convenient crypto tax calculator, which can help save you time filling out your IRS forms and ensure you complete your tax filing correctly.

When calculating your crypto taxes, it’s essential to keep track of your cost basis, this refers to the fair market value of your assets when you acquire them. If you’ve bought the same crypto multiple times, you’ll need to apply the FIFO (First In, First Out) method to calculate your cost basis. This means the first assets you buy are the first assets you sell when preparing your tax filing.

Crypto Tax Losses

What a wonderful world it would be if we only experienced crypto gains and avoided losses entirely. Unfortunately, no one has a 100% hit rate when crypto trading, and suffering a few red candles is inevitable.

The good news is that you can declare your losses to reduce your tax liability. This is called tax-loss harvesting and is a standard method for traders and investors to offset their capital gains tax payments.

To get a better understanding of how tax-loss harvesting works in crypto, take this imaginary example:

- You buy one BTC at $20,000 and one ETH at $1,000.

- While you hold both assets, ETH pumps to $2,000, while BTC falls to $19,500.

- You sell your ETH for $2000, earning $1,000 in profit.

- You sell your BTC for $19,500, realizing a $500 loss.

If you don’t sell your BTC and realize capital losses, you will need to pay capital gains tax on the $1,000 you earnt trading ETH. However, because you’ve registered a $500 loss on BTC, you can offset that loss against your gains. As a result, you only need to pay tax on $500 earned in your ETH trade instead of $1,000.

On The Flip Side

- Crypto taxation and regulations are under constant scrutiny and revision worldwide. Every country has difficult crypto tax laws that are prone to frequent change. You should always stay up to date on your local crypto regulation standards and consult a tax professional or certified public account (CPA) when managing your taxes.

Why Should You Care

Avoiding your crypto tax reporting responsibilities could land you in hot water with your local jurisdiction. Staying informed on how to pay your crypto tax correctly will save you a lot of headaches at the end of every tax year.

FAQs

Yes, you should always report any crypto gains or income earned from cryptocurrency transactions in your tax preparation. Failure to do so could result in tax evasion charges from your local governing body.

No, in most circumstances, you only need to pay tax on cryptocurrency when you realize capital gains or earn income from crypto transactions.

Yes, you can write off crypto losses and reduce your tax bill by offsetting your profits against capital losses. This is called tax-loss harvesting and can be a complicated procedure. We recommend consulting a tax professional when filing your tax reports.

Countries like the United Arab Emirates (Dubai), Singapore, and Portugal have some of the most lenient crypto tax laws. This makes these locations a popular country of residence for crypto investors and traders.

No, buying Bitcoin or any other cryptocurrency is not considered a taxable event. However, the moment you choose to sell or dispose of the asset is a taxable event and must be correctly registered.