- The FDIC has reported ongoing, significant unrealized losses for the U.S. banking sector.

- The 2023 banking crisis was a boon for the Bitcoin price.

- Some industry figures predict Bitcoin will thrive in an economic crisis.

Bitcoin is the best-performing asset this decade, recording a staggering 9,000,000% increase since 2011, leaving the Nasdaq’s 617% returns over the same period in the dust. To date, BTC is up 64% since the start of 2024 and has been hovering around the $70,000 mark for the past few weeks.

Despite the lull in price action, some industry figures, such as Samson Mow, Jack Mallers, and Arthur Hayes, believe BTC could soar as high as $1 million this bull cycle, an extremely lofty target even in the best-case scenario.

Sponsored

However, proponents of a $1 million BTC state that this would come at the cost of an economic catastrophe, with the resulting flight to safety driving up BTC’s price. The latest Federal Deposit Insurance Corporation (FDIC) report paints a troubling outlook, potentially validating such concerns.

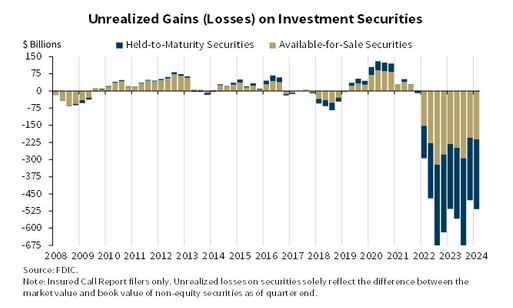

FDIC Report Points to Brewing Crisis

The FDIC’s Q1 report gave insight into the condition and performance of the U.S. banking industry, with concerns raised over losses on securities. The report revealed that unrealized losses on securities increased by $39 billion to $517 billion during the quarter. These losses were largely driven by higher unrealized losses on residential mortgage-backed securities, resulting from the impact of higher mortgage rates.

Notably, Q1 marked the ninth consecutive quarter of unrealized losses on securities for the banking industry, a concerning trend that kicked off following the Fed’s first hiking rates in Q1 2022.

Adding to the woes, the FDIC has increased the number of banks on its “Problem Bank List” to 63 in Q1, up from 52 in the previous quarter. Problem banks are institutions deemed at risk of collapse due to financial, operational, and managerial weaknesses.

The growing number of problem banks and the persistent unrealized losses on securities highlight the mounting stress on the banking sector, raising concerns about its stability and resilience in the face of ongoing economic challenges.

Bitcoin to Moon?

The U.S. banking crisis, which began in March 2023 leading to the collapse of Silicon Valley Bank, Silvergate, and Signature Bank, coincided with a 40% surge in the Bitcoin price over seven days. This price action added to the narrative that BTC is an uncorrelated asset class, serving as a flight to safety amid banking and economic instability.

Vijay Ayyar, vice president of corporate development at Luna, echoed this sentiment at the time, stating, “If one looks at the history of bitcoin and why it was created in the first place, it was precisely for events like this where the current system shows signs of weakness, and hence owning an uncorrelated asset helps.”

Although the money supply has been contracting since early 2021, Bitcoin bull Willy Woo noted that the M2 money supply has recently ticked up above 0% to 0.7%. Historically, periods of M2 monetary expansion have coincided with increases in the BTC price.

With U.S. banks showing signs of weakness, many wonder if aggressive money printing by the Fed to prop up the economy is inevitable, potentially driving more capital into Bitcoin as a hedge against currency debasement.

On the Flipside

- BTC‘s correlation with other assets is dynamic, going through periods of weak to strong correlation.

- The FDIC report also noted improvements, such as net quarterly income increasing 79.5% to $64.2 billion versus the prior quarter.

Why This Matters

The FDIC’s report revealing growing strains in the banking sector underscores Bitcoin’s value proposition as a non-sovereign, fixed-supply asset. However, BTC at $1 million seems an extraordinary claim at this point.

The American Bankers Association shows surprising support for cryptocurrency.

U.S. Banking Lobby Made Last-Ditch Effort to Block SAB 121 Veto

Peter Brandt gives his take on the peak BTC price and when it may top this cycle.

Brandt Predicts Bitcoin Top with Halving Analysis