- The Bitcoin halving in April continues to reshape the mining landscape.

- Miners are being squeezed under current conditions.

- The ‘HODL tax’ was suggested as a solution for miners’ woes.

Miners form the backbone of the Bitcoin network, validating transactions and ensuring the integrity of the blockchain. Under this model, miners earn block rewards and fees by competing to guess the target hash to win the block. The mining difficulty adjusts based on the current level of competition, ensuring the network remains secure and efficient.

However, nearly three months after the halving, miners are struggling to stay afloat and are leaving the network. Last week saw a significant drop in mining difficulty, signaling that many are shutting down their rigs and exiting the industry. This trend raises critical questions about the long-term sustainability of Bitcoin mining in the current landscape.

Bitcoin Miners Feeling the Pinch

Bitcoin mining sustainability is under scrutiny after another major drop in difficulty, indicating that miners are shutting down their rigs as they struggle to stay profitable.

Sponsored

According to CoinWarz, mining difficulty decreased by 5%, falling from 83.68 T to 79.5 T on July 5. This marked the second major decline since the halving event on April 20. The first substantial drop post-halving occurred on May 10, when difficulty decreased by 5.6% from 88.1 T to 83.15 T.

While there have been minor fluctuations between these two major drops, the overall trend post-halving points towards a downward trajectory in difficulty.

Bitcoin’s difficulty adjustment mechanism, which occurs every 2,106 blocks (approximately every two weeks), aims to maintain a consistent block production rate of one new block every 10 minutes.

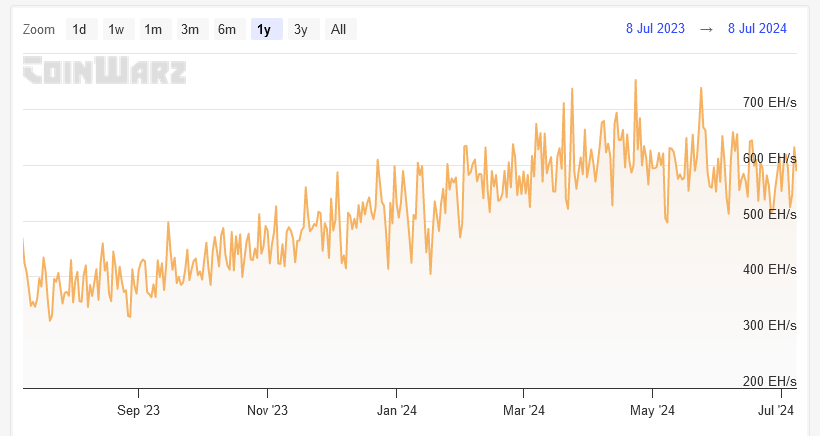

The drop in mining difficulty parallels a decline in hash rate, the network’s total computational power. After peaking at a record 751.63 EH/s on April 23, the hash rate has been steadily falling and now sits at 607.8 EH/s.

Daily revenue figures for Bitcoin miners tell a similar story of struggle. On the day of the halving, April 20, miners’ daily revenue peaked at an all-time high of $107.8 million. However, this figure has since plummeted, hitting a local bottom of $22.3 million on July 5.

Miners’ post-halving struggles have led to the HODL tax proposal as a potential solution.

HODL Tax Falls Flat

In response to the growing challenges faced by miners, a July 4 opinion piece in Bitcoin Magazine proposed a HODL tax for long-term holders. This tax aims to boost mining revenue by encouraging more network activity.

Under the proposal, addresses inactive for over a year would incur automatic BTC deductions, which would then be redistributed to miners. The deduction would be set at 50% of the median transaction fee from the previous two weeks.

Despite its intent, the HODL tax has faced significant backlash from the Bitcoin community. Critics argue that it disrupts the fundamental incentive to buy Bitcoin, which currently offers zero carrying costs.

On the Flipside

- Bitcoin miners require cheap electricity to be profitable.

- While renewable energy sources are often touted as the best fit for miners, nuclear power is becoming more prevalent.

- Observers predict greater consolidation of miners as they continue to struggle, raising concerns about decentralization.

Why This Matters

Bitcoin miners’ current struggles highlight potential sustainability issues with the current mining model, particularly as future halvings will further reduce rewards.

The continued Bitcoin sell-off sparks fears that the bear market has returned:

Bitcoin Bull Run Stumbles: Will $50,000 Hold?

Cardano joins the Inter-Blockchain Communication alliance for greater interoperability:

How Cardano Joining IBC Amps up Sidechain Connectivity